Africa is home to 50+ countries and 40+ currencies.

Moving money across its borders — for both intra-African and global trade — means navigating fragmented banking systems, volatile exchange rates, scarce dollar liquidity, and correspondent banking chains that route even intra-African payments through New York or London.

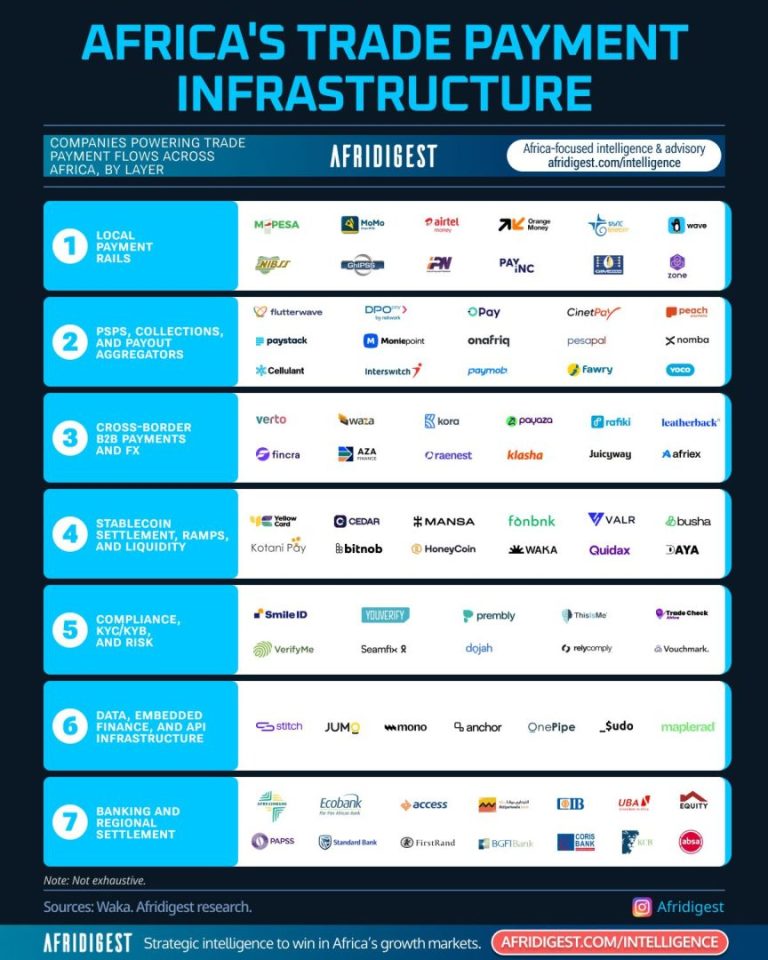

Here’s a look at the infrastructure powering how money moves for African trade, from last-mile rails all the way up to large-scale institutional settlement:

- Local Payment Rails — the mobile money platforms, instant payment systems, and local switches that form the last-mile plumbing for domestic money movement

- PSPs, Collections & Payout Aggregators — the Flutterwaves, Paystacks, and Cellulants that sit on top of local rails and abstract them into APIs for businesses

- Cross-Border B2B Payments & FX — the corridor players routing money between markets for trade purposes (as opposed to consumer remittances)

- Stablecoin Settlement, Ramps & Liquidity — the fastest-growing layer, where digital assets (like dollar-pegged USDT or USDC) & blockchain networks are beginning to displace traditional infrastructure

- Compliance, KYC/KYB & Risk — the identity, verification, and security layer every transaction depends on

- Data, Embedded Finance & API Infrastructure — the developer-facing tools powering additional products & services

- Banking & Regional Settlement — the institutional backbone that anchors the system (often the final settlement layer even when stablecoins or fintechs are involved upstream)

Some companies operate in multiple layers, and no single layer solves cross-border trade payments alone.

A Nigerian manufacturer paying a Kenyan supplier might touch four or five of these layers in one transaction: local rails to collect naira, a PSP or aggregator to convert and route it, an FX/B2B corridor player to get it into shillings, and a bank to settle the final leg — with compliance and identity checks running underneath the entire chain.

That fragmentation is a reflection of the underlying reality of African markets — with distinct regulatory regimes, central banks, licensing requirements, and liquidity constraints.

The most interesting shift right now is happening at the intersection of Layers 3 and 4 — where stablecoin-native platforms are beginning to challenge traditional cross-border FX rails on speed, cost, and accessibility.

A traditional correspondent-banking transfer between African markets typically takes two to five business days to settle, sometimes longer on certain corridors, as payments get routed through intermediary banks — often in New York or London — even for purely intra-African transactions, with fees stacking at hop.

A stablecoin-settled transaction can clear in a fraction of the time at a fraction of the cost, bypassing the intermediary chain and giving businesses in dollar-scarce markets a way to hold and move dollar-denominated value without waiting on thin local FX liquidity.

What’s not yet proven at scale: regulatory clarity varies sharply by country, on/off-ramp liquidity is still shallow outside a handful of corridors, and enterprise treasury teams are still building the trust and compliance infrastructure needed to hold digital assets on balance sheet. That said, stablecoin-powered and stablecoin-native platforms in Layer 4 are rapidly becoming formidable contributors to trade payments across the continent.

Every layer in this stack exists because Africa’s payment infrastructure is still, fundamentally, 50+ separate systems learning to talk to each other. The winners at each layer will be the ones who make that fragmentation invisible to the businesses actually trying to move money.

Share: